What Is Asset Turnover Ratio?

Asset Turnover Ratio: The asset turnover ratio measures the value of a company’s sales or revenues relative to the value of its assets. The asset turnover ratio can be used as an indicator of the efficiency with which a company is using its assets to generate revenue. The higher the asset turnover ratio, the more efficient a company. Conversely, if a company has a low asset turnover ratio, it indicates it is not efficiently using its assets to generate sales.

In certain sectors, asset turnover tends to be higher for companies than in others. For example, retail companies have relatively small asset bases combined with high sales volume. This leads to a high average asset turnover.

Meanwhile, firms in sectors such as utilities tend to have large asset bases and low asset turnover. Selling off assets to prepare for declining growth has the effect of artificially inflating the ratio. Comparisons carry the most meaning when they are made for different companies within the same sector.

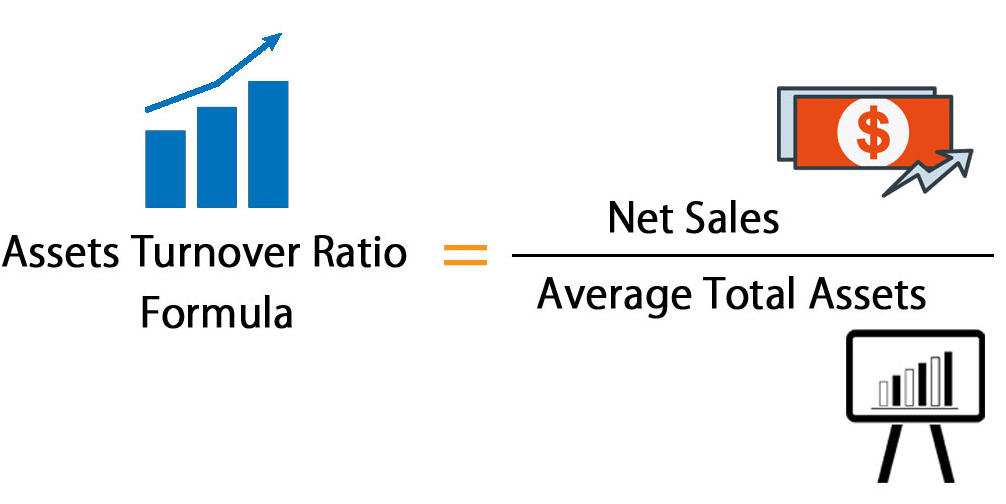

Asset Turnover Ratio Formula

The asset turnover is calculated by dividing net sales by average total assets.

Net sales, found on the income statement, are used to calculate this ratio returns and refunds must be backed out of total sales to measure the truly measure the firm’s assets’ ability to generate sales.

Read Also: Capital One Business Checking?

Average total assets are usually calculated by adding the beginning and ending total asset balances together and dividing by two. This is just a simple average based on a two-year balance sheet. A more in-depth, weighted average calculation can be used, but it is not necessary.

Total Asset Turnover Ratio

The total asset turnover compares the sales of a company to its asset base. The ratio measures the ability of an organization to efficiently produce sales and is typically used by third parties to evaluate the operations of a business. Ideally, a company with a high total asset turnover can operate with fewer assets than a less efficient competitor, and so requires less debt and equity to operate. The result should be a comparatively greater return to its shareholders.

The formula for total asset turnover is:

Net sales ÷ Total assets = Total asset turnover

For example, a business that has net sales of $10,000,000 and total assets of $5,000,000 has a total asset turnover of 2.0. This calculation is usually performed on an annual basis.

It is best to plot the ratio on a trend line, to spot significant changes over time. Also, compare it to the same ratio for competitors, which can indicate which other companies are being more efficient in wringing more sales from their assets.

There are several problems with the ratio, which are:

-

The measure assumes that additional sales are good when in reality the true measure of performance is the ability to generate a profit from sales. Thus, a high turnover ratio does not necessarily result in more profits.

-

The ratio is only useful in the more capital-intensive industries, usually involving the production of goods. A services industry typically has a far smaller asset base, which makes the ratio less relevant.

-

A company may have chosen to outsource its production facilities, in which case it has a much lower asset base than its competitors. This can result in a much higher turnover level, even if the company is no more profitable than its competitors.

-

A company may be penalized for deliberately increasing its assets to improve its competitive posture, such as by increasing inventory levels in order to fulfill more customer orders within a short period of time.

-

The denominator includes accumulated depreciation, which varies based on a company’s policy regarding the use of accelerated depreciation. This has nothing to do with actual performance but can skew the results of the measurement.

In general, the return on assets measure is better than the total asset turnover, since it places the emphasis on profits, rather than sales.

Fixed Asset Turnover Ratio

This ratio measures how efficiently a firm uses its assets to generate sales, so a higher ratio is always more favorable. Higher turnover ratios mean the company is using its assets more efficiently. Lower ratios mean that the company isn’t using its assets efficiently and most likely have management or production problems.

For instance, a ratio of 1 means that the net sales of a company equal the average total assets for the year. In other words, the company is generating 1 dollar of sales for every dollar invested in assets.

Like with most ratios, the asset turnover ratio is based on industry standards. Some industries use assets more efficiently than others. To get a true sense of how well a company’s assets are being used, it must be compared to other companies in its industry.

The total asset turnover ratio is a general efficiency ratio that measures how efficiently a company uses all of its assets. This gives investors and creditors an idea of how a company is managed and uses its assets to produce products and sales.

Sometimes investors also want to see how companies use more specific assets like fixed assets and current assets. The fixed asset turnover ratio and the working capital ratio are turnover ratios similar to the asset turnover ratio that is often used to calculate the efficiency of these asset classes.

Fixed Asset Turnover Ratio Formula

The asset turnover ratio measures the efficiency of how a company uses assets to produce sales. A higher ratio is favorable, as it indicates a more efficient use of assets. Conversely, a lower ratio indicates the company is not using assets as efficiently. This can be due to excess production capacity, poor collection methods, or poor inventory management.

Read Also: EBITDA formula

It is important to compare the ratios between companies operating in the same industry, as the benchmark asset turnover ratio varies greatly depending on the industry. Industries with low-profit margins tend to generate a higher ratio and capital-intensive industries tend to report a lower ratio.

Asset Turnover Ratio Calculator

To calculate the asset turnover ratio, divide net sales or revenue by the average total assets. For example, suppose company ABC had total revenue of $10 billion at the end of its fiscal year. Its total assets were $3 billion at the beginning of the fiscal year and $5 billion at the end. The average total assets are: $8 billion ($3 billion + $5 billion) ÷ 2 or $4 billion. Its asset turnover ratio for the fiscal year is 2.5 (that is, $10 billion ÷ $4 billion).